We have a huge opportunity to enable the energy transition and SAVE MONEY. If we reduce Primary Nickel use in stainless steels, we can have a big influence on the price and availability of Nickel for batteries, electrolysers etc., and also promote the cost effective use of stainless steels. It will also make big reductions in CO₂e emissions.

Critical minerals are big news. The major global powers are scrambling to control territory where they are, or could be, mined and processed. Major studies have reported [1], [2], [3] on the complexities of prospective demand and supply, and the grave implications for our peace, prosperity, and the viability of human civilization.

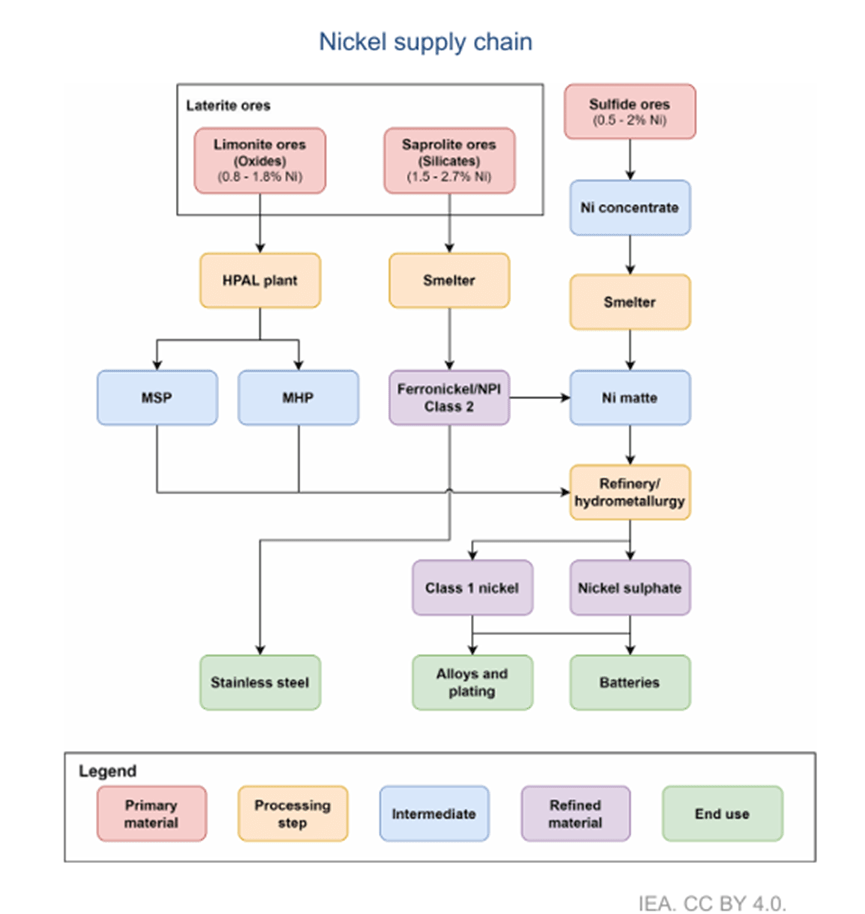

Nickel is regarded as a Critical or Strategic Material with rapidly growing demand, most prominently driven by the growth in demand for Lithium Ion Batteries (LIB) for electric vehicles (EV), although in 2024 65% of the 3.5 Million Tonnes of Primary Nickel production was still used to make stainless steels (STS). Fig. 1 shows a schematic diagram of the main Nickel supply chains.

Fig. 1 International Energy Agency [1]: Main Nickel Supply Chains

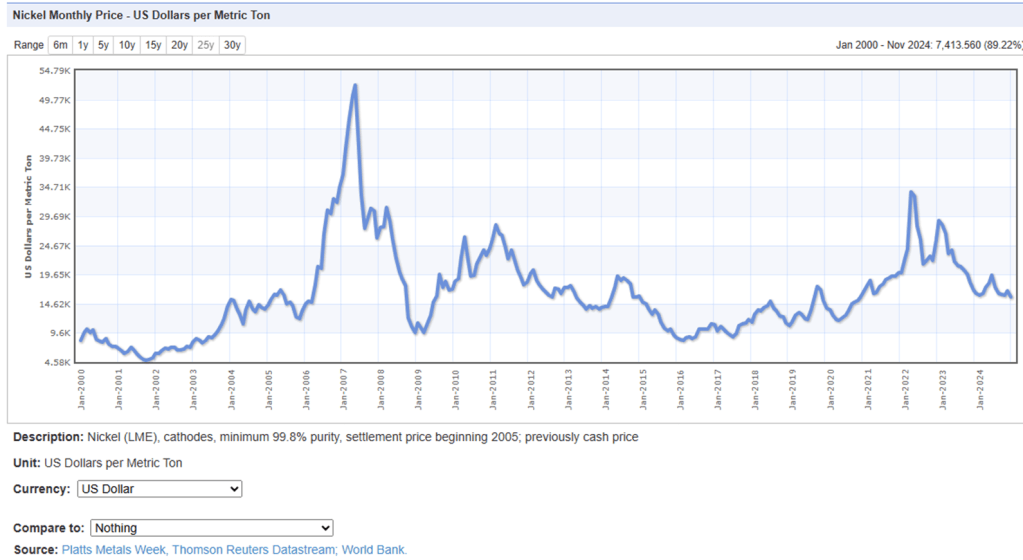

In 2023 and 2024 there has been a surplus in Primary Nickel supply over demand, resulting in the LME price settling around $15k to $16k per Tonne and the closure of some high cost mines. Historically, shortages of Nickel have driven the LME price to $30 or even $50k/Tonne – see Fig. 2.

Fig. 2 Index Mundi [4]: Historical Ni Prices

References.

[1] ‘’Global Critical Minerals Outlook 2024’’ International Energy Agency.

[2] ‘’Materials and Resource Requirements for the Energy Transition’’ Version 1.0, July 2023, The Energy Transition Commission.

[3] ‘’Critical Minerals and Great Power Competition, An Overview’’ Oct 2024, The Stockholm International Peace Research Institute.

[4] ‘’Historical Nickel Prices’’ Index Mundi [https://indexmundi.com/commodities]